- The technology-driven stock market rally is on the verge of rivaling market bubbles not seen since the dot-com era and the Great Depression, according to Stifel’s Barry Bannister.

- The only way stocks can move “sharply higher” from current levels is if a bubble is formed, fueled by near-zero interest rates and a falling equity risk premium, Bannister said.

- Bannister nailed last week’s market sell-off, having called the market 5% to 10% overvalued just last month.

- Visit Business Insider’s homepage for more stories.

Investors still have a lot to learn from the Nifty Fifty stock market bubble of 1972 and the dot-com bubble of 2000, according to Stifel’s Barry Bannister.

In a recent note to clients, the head of institutional equity strategy said the current technology-driven stock market was showing similarities to previous market bubbles and was even rivaling past melt-ups based on the cyclically adjusted price-earnings ratio, or CAPE.

“The current market level is pivotal,” Bannister said, adding: “The CAPE of the S&P 500 is knocking at the doorstep of the same point at which CAPE broke out in the last two years of the most powerful bull markets of the past century, the late 1920s and late 1990s.”

If the widely followed CAPE ratio does break above the 30-times level and move decisively higher, “the building and bursting of a bubble” could occur, according to the note.

"The only path we see to a sharply higher market is a bubble like the end-stage of the 1920s and the 1990s bull markets," the note said.

Fueling a continued rally in stocks would be near-zero interest rates and a falling equity risk premium. In other words, the monetary policies from the Federal Reserve will most likely be the determining factor of how long the stock market rally can last.

According to Bannister, the S&P 500 could soar if Fed Chair Jerome Powell is able to avoid the taper tantrum of 2013 and suppress the real 10-year Treasury yield. In this scenario, the S&P 500 could jump 10% from current levels to 3,700, Stifel said.

Additionally, there is a "mega-bull case" for stocks, depending on how low the real 10-year Treasury yield can fall, Bannister said. The real 10-year Treasury yield is the current interest rate of the 10-year Treasury less the current rate of inflation.

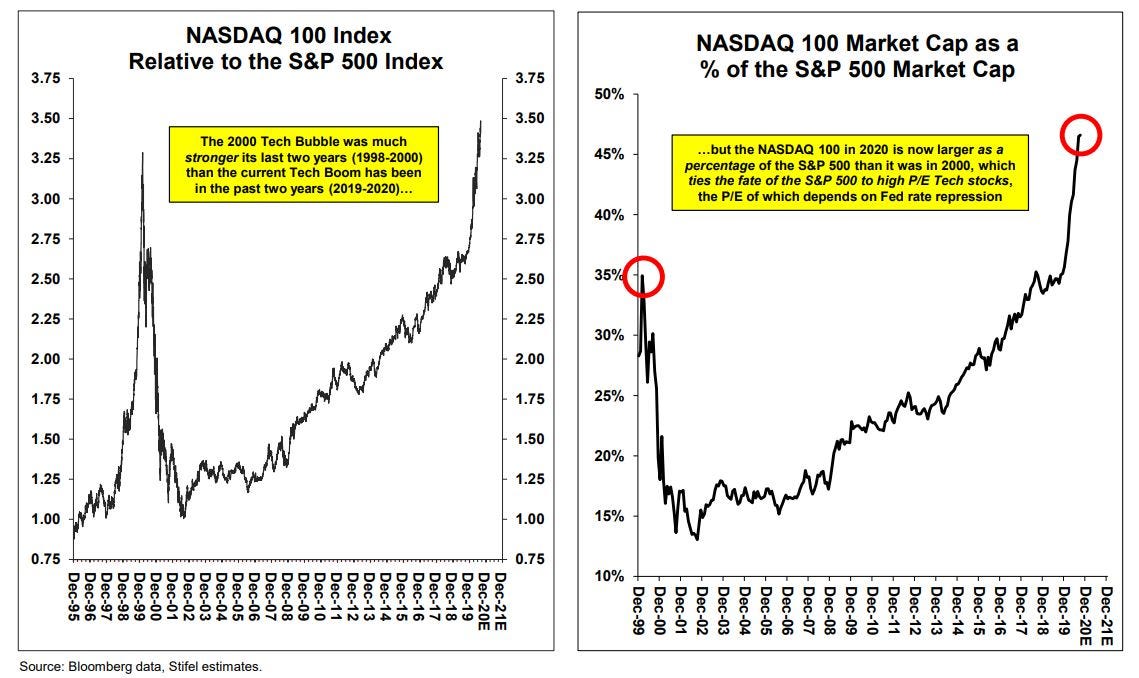

Still, market valuations are "precariously high" and investors should note that the decade following the dot-com bubble led to underperforming tech stocks relative to the S&P 500 despite faster earnings growth, the note said.

Investors should take note of Bannister's call. The Wall Street strategist wasn't surprised by this week's tech-driven market sell-off given his note last month called for a 5% to 10% market pullback.